Harvesting

Trees grow at different rates, so harvesting an entire plantation may take from 1 to 3 years depending on the site variation and harvest management strategy. Some growers prefer to cut and market an entire crop in one year. This technique requires an extra year or two to allow a greater number of trees to reach marketable size. Trees still too small for market are either cut into boughs or destroyed. An advantage of this method is the lower cost of harvesting and clearing the area for replanting.The predominant strategy is to harvest for several years on an area as the trees reach saleable size. This method produces a greater yield of trees per acre, but increases harvesting costs and possible delays in replanting that may offset the increased profits.

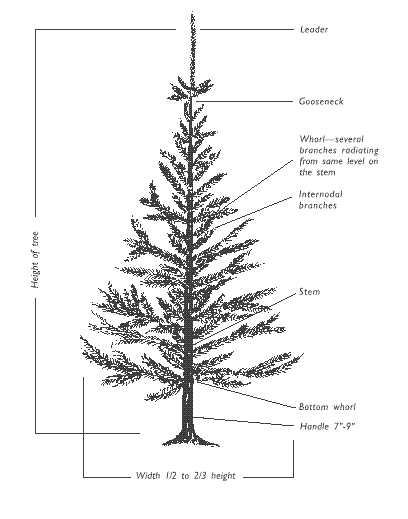

In harvesting for a wholesale market, trees should be cut with a sharp saw at right angles to the stem to leave a flat base. The person responsible for designating the trees to be cut should be familiar with market specifications, such as height, straightness of stem, length of handle, symmetry, and fullness of foliage.

Trees should be carried (not dragged) to a specified packaging and loading area. Twine or a plastic netting may be used to bundle or "bale" trees. Trees can be packaged by a baling machine or by using a simple cone through which trees can be pulled to constrict them for tying. Packaging trees in this manner can reduce damage during handling and shipping. Trees should then be hauled to the nearest truck-loading point and sorted according to species, height, and quality as they are unloaded. Preliminary sorting reduces "wear and tear" of the trees when buyers want to inspect their trees at the loading point.

When trees are cut in advance of shipping date, loss of moisture may result in a lower quality product. Trees should be protected from direct sun and drying winds during the waiting period. Growers may find it profitable to hire additional labor at harvest time for simultaneous cutting and loading operations. While this practice increases handling costs, it avoids delaying truckers waiting for the trees.Marketing

The marketplace is where the grower learns whether the money and effort expended to produce quality trees is enough to allow profitable competition against artificial trees and trees grown in other areas.Marketing methods vary according to the size of operations and the buyers' demands for quality and other services. While the majority of North Carolina growers sell trees on a wholesale basis, a number of choose-and-cut farms are also in operation. Many of the same principles of marketing apply regardless of selling method.

A grower's reputation for selling quality trees year after year can reduce the buyers need to inspect the trees at the plantation. A good reputation can thereby facilitate marketing and help retain satisfied customers.

Growers should label trees accurately according to species, height, and general quality in terms of color, density, and shape. This procedure helps to build a good seller-buyer relationship. A brochure listing salable trees sent to all prospective buyers can help to increase sales. Such a brochure should include the species, size, quality, selling method (on the stump, at roadside, or delivered) and expected price. Growers may help sales by including pictures of their plantations and individual trees.

Many wholesale growers cut and harvest their own trees, but in some instances they may tag their trees and let the buyers do the cutting. It is usually better for the grower to harvest in order to retain control and prevent high-grading and physical damage to the plantation.

When cutting many trees for specific buyers, it would be advisable to have a performance contract signed by part of the marketing risk and offering additional services, growers can expect a better net price per tree.

Some growers who live near population centers sell trees directly to consumers from the plantation as choose and cut. This method requires adequate all-weather parking in an accessible area within close driving distance of the city. Signs should be strategically located so that customers can find the plantation without difficulty. Thieves can also follow these directions, so there may be an increased need for security. Sales are frequently increased by advertising the location of a plantation and hours of operation. Customers should be provided with tools or assistance to cut their choice from among several species of trees on several acres. Growers should carry liability insurance.

There is considerable risk in retailing Christmas trees. The retailer's margin need not be as high if the grower assumes part of the risk. For example a grower could absorb all or a part of the loss on unsold Christmas trees, or deliver trees as the retailer needs them. This decreases the possibility of having large numbers of cut trees on hand after Christmas.

United States Department of Agriculture standard grades for Christmas trees may be used as a guide in grading trees for sale. If both grower and buyer know these standard grades and accept them, tree sales can be made by phone or letter without an "on the ground" inspection.

Growers and buyers often find it beneficial to join Christmas tree associations. Many production and sales techniques can be obtained at regular association meetings. Helpful information can also be found in the associations' periodic newsletters and publications.Record Keeping

Complete, documented records are essential to any business, including Christmas tree production. Records should include a map of the farm layout, with fields, roads, topography, drainage systems, species and number of trees per field, and planting dates clearly designated.Other records should include soil test data, weather conditions at the time of planting, pest and weed control efforts, and detailed cost and return figures. Data should also be maintained concerning trees survival of transplant shock, mowing machine injury, and pest infestations. A continuous inventory of salable trees permits calculation of cost per tree, or fertilizer and pest control chemicals needed, and depletion allowance. Records should contain information detailed enough to permit determination of the weak points of the total operation. The records also enable growers to compare their costs with published estimates.

Records are also useful in determining a cash basis needed to arrive at capital gains for use in casualty loss, damage claims, sale of property, or a fair market value for estate tax purposes. Accurate cost records can prevent payment of unnecessary taxes.Investment Planning

Before investing in a long-term crop like Christmas trees, the cost of production must be carefully weighed against the intended level of investment. Additionally, once a grower is in full production with trees at all stages of growth, there is a common progression of practices that add up to the total cost of production for any year.Table 5. Labor, total expenses, and income generated

by 1 acre of Fraser fir Christmas trees

| Year | Labor (Hours) | Total Expenses | Gross Income |

| Year 0 | 6.1 | $ 1,087.07 | — |

| Year 1 | 68.2 | $ 1,939.70 | — |

| Year 2 | 34.8 | $ 885.96 | — |

| Year 3 | 34.0 | $ 896.41 | — |

| Year 4 | 41.2 | $ 986.16 | — |

| Year 5 | 44.2 | $ 1,178.23 | — |

| Year 6 | 112.2 | $ 2,043.71 | $ 7,400.00 |

| Year 7 | 151.2 | $ 2,695.06 | $16,900.00 |

| Year 8 | 75.8 | $ 1,640.82 | $ 9,150.00 |

| TOTALS | 567.7 | $13,353.12 | $33,450.00 |

| Net Income | $20,096.88 | ||

| Net Annual Income (Net/8 yr) | $2,512.11 | ||

| Total Establishment and Growing Costs after Year 5 | $6,973.53 | ||

Table 5 indicates the labor required, total expenses, and proceeds to be anticipated for one acre of Fraser fir Christmas trees over an 8-year rotation. Table 6 provides an example of common operations conducted during the year and their cost. Costs will vary with location, weather, tree species, availability of labor, and variations, in supplies and equipment.

Table 6. Common Christmas tree production operations and their cost range by acre.

| Operation | Cost /Acre | Operation | Cost /Acre |

| Purchase land | $ 500-5000 | Liquid insecticide application | $ 100-300 |

| Site preparation | $ 200-1000 | Mowing between trees | $ 20-40 |

| Tractor applied lime | $ 25-50 | Mowing farm roads | $ 10-20 |

| Tractor applied fertilizer | $ 50-100 | Manual shearing | $ 200-450 |

| Mechanical tree planting | $1,500-2,000 | Tagging market trees | $ 25-50 |

| Hand setting replants | $ 100-500 | Cutting trees (500) | $ 50-100 |

| Manual lime or gypsum application | $ 30-60 | Baling trees (500) | $ 250-500 |

| Manual herbicide application | $ 15-40 | Storing trees (500) | $ 40-100 |

| Manual fertilizer application | $ 40-80 | Loading trees (500) | $ 40-80 |

| Granular insecticide application | $ 40-50 |

Most budgets are for one acre over the course of a rotation. This approach can be potentially misleading. Most growers plant annually and eventually harvest annually. However, others increase the acreage planted each year as their expertise and goals for future income increase. Table 7 expands the single-acre values from Tables 5 and 6 into an example of a 9-acre farm with 1 acre planted annually. As total production acreage and the number of older trees accumulate, annual costs will increase. Income from initial plantings usually is rolled back into the business to sustain a higher future level of production. Frequently, the break-even point may not occur until well into the second production cycle.

Table 7. Cash flow chart for a 9-acre Fraser fir Christmas tree farm (1 acre planted annually)

| Year 1 | Year2 | Year 3 | Year 4 | Year 5 | Year 6 | Year 7 | Year 8 | Year 9 | |

| 1 acre | $1,087 | $1,940 | $ 886 | $ 896 | $ 986 | $1,178 | $2,044 | $2,695 | $1,641 |

| 1 acre | $1,087 | $1,940 | $ 886 | $ 896 | $ 986 | $1,178 | $2,044 | $2,695 | |

| 1 acre | $1,087 | $1,940 | $ 886 | $ 896 | $ 986 | $1,178 | $2,044 | ||

| 1 acre | $1,087 | $1,940 | $ 886 | $ 896 | $ 986 | $1,178 | |||

| 1 acre | $1,087 | $1,940 | $ 886 | $ 896 | $ 986 | ||||

| 1 acre | $1,087 | $1,940 | $ 886 | $ 896 | |||||

| 1 acre | $1,087 | $1,940 | $ 886 | ||||||

| 1 acre | $1,087 | $1,940 | |||||||

| 1 acre | $1,087 | ||||||||

| Cost | $1,087 | $3,027 | $3,913 | $4,809 | $5,795 | $6,973 | $9,017 | $11,712 | $13,353 |

| Income | $7,400 | $24,300 | $33,450 | ||||||

| Net | –$1,087 | –$4,114 | –$8,027 | –$12,836 | –$18,631 | –$25,604 | –$27,221 | –$14,633 | +$5,464 |

| (net is cumulative over rotation) Break-even Point for a 9- Acre Farm: Year 9 Total Cost of Production for 9 Acres (over 17 years): $120,177 Total Income for 9 Acres (over 17 years): $301,050 Net Income for 9 Acres (with no 2nd rotation): $180,873 | |||||||||

Taxes

It is beyond the scope of this publication to get into a detailed analysis of record keeping or tax treatment of both the buyer and seller. Usual terms call for a one-third payment when the contract is signed and the balance paid when the trees are picked up.Growers with large acreage are obliged to move thousands of trees. With efficient management, their production costs per tree may be less than growers producing smaller numbers of trees. However, growers with fewer trees may have more flexibility, and can take advantage of customer service requirements, such as selling either at the plantation or delivering trees directly to specific retailers.

To realize a fair return, growers with small areas may compete with those having larger acreage by improving efficiency of operations, offering a better quality product, and reliably supplying specific retail markets. They may also compete with those offering larger volumes by combining sales of trees with other growers.

Many growers operate their own retail lot and market their own trees. Those selling fewer trees may offer additional services, such as letting a buyer select and cut his own trees and making sales on consignment. By accepting timber sale income and expenses. However, there are some basics of this topic that should be considered.

Establishment costs include any costs associated with site preparation and practices necessary to ensure tree survival. Included are land preparation, lime, fertilizer, herbicide, interest, hired labor, tools, seedlings, and depreciation deductions on equipment used for any of these activities. Establishment costs are recorded in a capital account, and these costs are recovered on a per tree harvested basis (depletion) when the trees are sold.

Growing period costs begin after trees are established. Included are hired labor, fertilization, weed control, shearing and shaping, insect and disease control, rental payments, interest on production loans, road and fireline maintenance, and depreciation deductions on equipment used for any of these activities. Growing period costs would normally be deducted each year. To be eligible to deduct these expenses, a grower must be considered a material participant in a trade or business. The Internal Revenue Service publishes a series of criteria that must be met in order to be considered a material participant.

Most growers would benefit by deducting growing period expenses annually. If a grower does not qualify as a material participant in a trade or business, the operation is defined as a passive activity. Deductions from passive activities are allowed only to the extent of total passive income from all passive activities for the tax year. Growing period costs not deducted annually may be carried forward and recovered through depletion at the time of sale or until there is passive income from some source in the case of passive activities. A growing period cost accountshould be maintained and adjusted as costs are incurred or deducted.

Sales costs can be deducted from the sale proceeds. Examples are tree marking, harvesting, bagging or baling, hauling, advertising, and hired labor.

Gains and losses from the sale of Christmas trees can qualify for special tax treatment as capital gain or capital losses. An evergreen tree that is more than 6 years of age when it is severed from its roots and sold is considered by the Internal Revenue Service Code to be timber with sales treated as capital gains income (loss). Age is calculated from the time of seed germination. If trees are not 6 years old or are dug and sold as live trees, then they are considered to be horticultural products and the sales are treated as ordinary income (loss). The advantage of selling Christmas trees as timber is that the highest marginal tax rate on long-term capital gains is historically less than the highest marginal tax rate on ordinary income. Also, capital gains income is not subject to self-employment taxes as is ordinary income.

Selling method is also important if the sale is to qualify as the sale of a capital asset (timber). Methods are: 1) cutting of standing timber with an election to treat as a sale; or 2) disposal of timber with an economic interest retained.

For questions regarding tax laws, growers are advised to enlist the services of a certified public accountant.Assistance Available

The North Carolina Cooperative Extension Service is a cooperative effort among the United States Department of Agriculture, North Carolina State University, North Carolina A&T State University and county governments. Through the Extension Service, state and area specialists and county personnel can provide educational assistance, information, and guidance to the grower of Christmas trees.The North Carolina Forest Service is a service organization that provides planting stock and seedlings which may be grown as Christmas trees. Their foresters may assist with management advice about the culture of Christmas trees and pest control. The Division also assists landowners with fire control.

The North Carolina Department of Agriculture and Consumer Services (NCDA&CS) provides assistance to growers through the registration of appropriate pesticides and the providing of applicators licenses for those individuals using restricted-use pesticides. The NCDA&CS Agronomic Division provides both soil and tissue analysis with fertilization recommendations based on the results.

The Natural Resources Conservation Service (NRCS) of the United States Department of Agriculture is responsible for developing and implementing conservation programs. The NRCS can advise on site characteristics relative to soil and water, as well as suitability of tree species. The agency offers a varied amount of engineering assistance to growers in the management of water and soil resources.

Other government agencies, private companies, grower associations, etc., also provide beneficial information and services to Christmas tree growers.Summary

In growing Christmas trees as a business venture, the following points need to be given careful consideration:- Christmas tree crops require intensive management to produce a quality product. Unless a prospective grower is prepared to invest capital and many hours of labor in necessary management, it would be better to not start.

- Selection and preparation of planting sites are of critical importance. The topography, surface condition, elevation, exposure, internal drainage, and accessibility to roads should be carefully considered.

- Selection of tree species adapted to site conditions and those that have strong market appeal are important aspects to beginning a Christmas tree farm.

- Implementation of Integrated Pest Management and Best Management Practices will provide for efficient Christmas tree production while minimizing environmental impact.

- A grower must select good planting stock, take care of the trees, and plant properly to ensure maximum survival.

- Among the necessary cultural practices is a good pest control program, to include control of insects, diseases and unwanted vegetation.

- Trees must be shaped and sheared at the right time and at proper intervals to assure quality.

- Harvesting techniques must be adapted to a given situation to minimize damage and costs.

Christmas Tree Notes

Christmas Tree Terms

Note

This publication does not give specific information or suggestions concerning the use of pesticides for the control of insect, disease, or mite problems. The North Carolina Agricultural Chemicals Manual, which is revised annually, should be referred to for up-to-date pesticide information.Caution

Pesticides can be injurious to humans, domestic animals, desirable plants, and fish or other wildlife, if they are not handled or applied properly. Use all pesticides selectively and carefully and follow label instruction. Dispose of surplus pesticides and pesticide containers following recommended practices.Appendix

A Federal Income Tax Primer for North Carolina Christmas Tree Growers. North Carolina Cooperative Extension Service. North Carolina State University. Raleigh, NC.

American Christmas Tree Journal. Quarterly magazine of the National Christmas Tree Association, Inc., Milwaukee, WI.

Christmas Trees. Quarterly magazine published by Tree Publishers, Inc., Lecompton, KS.

Christmas Tree Notes. North Carolina Cooperative Extension Service. North Carolina State University. Raleigh, NC.

Christmas Tree Pest Manual. North Central Forest Experiment Station. USDA Forest Service. NE Area State and Private Forestry.

Christmas Tree Production Manual. Virginia Cooperative Extension Service. Virginia Polytechnic Institute & State University, Blacksburg, VA.

Identifying Seedling and Mature Weeds (AG-208). North Carolina Cooperative Extension Service. North Carolina State University. Raleigh, NC.

Limbs and Needles. Quarterly publication of the North Carolina Christmas Tree Association. Boone, NC

North Carolina Agricultural Chemicals Manual. College of Agriculture and Life Sciences. North Carolina State University. Raleigh, NC.

U. S. Department of Agriculture, Natural Resources Conservation Service,County Soil Survey Reports.

U. S. Department of Agriculture.United States Standards for Grades of Christmas Trees. USDA Agriculture Marketing Service. Revised 1989.